Personalized CX and digital experiences drive NPS in banking and financial services.

Personal banking is polarizing. Customers become enthusiastic promoters or disgruntled detractors of their financial institution, with few falling into passive middle ground, according to data from our recent UK consumer study, conducted in association with InMoment.

Why such strong feelings?

Consumers give their financial institutions loads of personal data. In exchange, they expect their banks to understand what’s happening in their lives and respond accordingly. Consumers expect banks to know what they need, exactly when they need it.

They also want to bank with minimal effort. In consumers’ minds, banks already have most of the information they need to open accounts or make lending decisions. Banking should be simple, especially online.

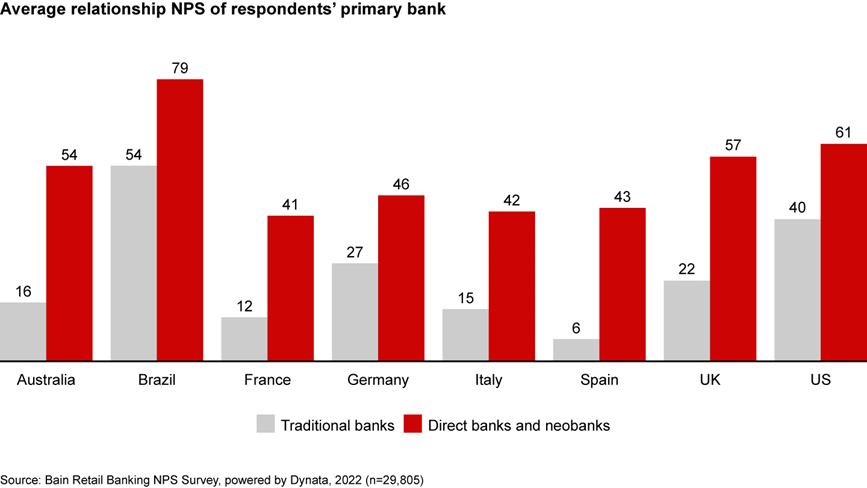

Traditional Banking is Falling Behind

Unfortunately, many traditional banks are falling behind their digital-first rivals in terms of customer satisfaction and customer experience (CX). According to a Bain survey on retail banking, neobanks in every country are outperforming their traditional counterparts in NPS.

It’s worth keeping score. Customers with stronger NPS scores stay longer, buy more, cost less to serve, and are more likely to recommend their banks to family and friends.

Plus:

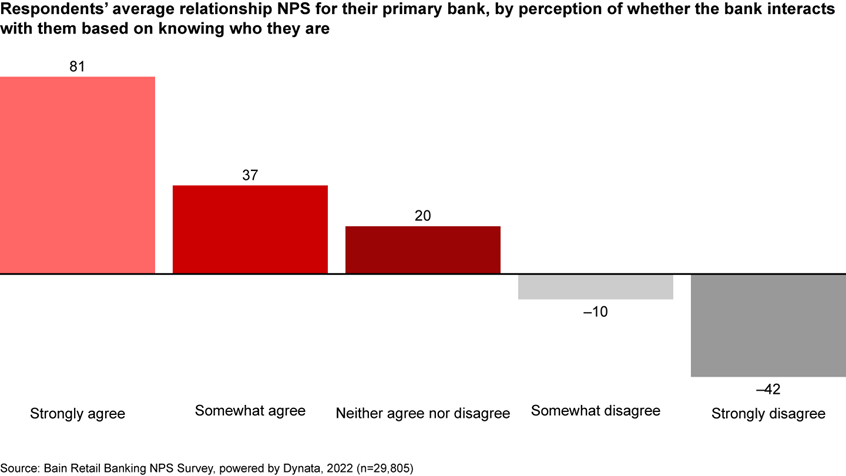

- There’s a 123-point difference in NPS between customers that feel like their bank interacts like they know them vs. those that don’t.

- Customers that successfully open a digital banking account the first time have an average NPS score of 50, compared to -53 for those who fail.

Customers seek advice and open accounts from financial institutions that deliver the best experience, without regard to tenure or physical features like branches and ATMs. Unless traditional banks intervene, neobanks will drain their share of wallet.

How to Get Customers to Fall in Love with Your Bank

Personalization and smooth digital experiences are driving loyalty in banking. To get customers to fall in love with your CX, start with these five steps:

- Collect the right data. With the right data, financial institutions can personalize banking services at scale. Collect information you need to personalize interactions and predict customers’ needs. This goes beyond knowing your customers. Look at payments data and cash flow patterns to anticipate individual customer’s money management needs and show them that you understand.

In examples Bain previously reported on in the UK, Halifax calls customers that seem to be in difficult financial situations. And RBC in Canada sends customers timely tips and personalized budgets. - Create granular customer segments. Form granular views of target customers using a combination of features. For a mortgage business, that could mean grouping customers based on type of community, financing structure, or other features that are statistically significant. Channel usage, brand preferences, and metrics from external data sources can also form useful clusters.

- Prioritize high-value customers. Lifetime value metrics can help you identify and rank target segments. Make sure segmentation accounts for customer value (not just volume), so you can prioritize CX strategies. This stops you from wasting time and resources retaining unprofitable customers.

- Become customer centric. Instead of focusing on what product you offer (e.g., credit cards or bank accounts), focus on the results. People take out lines of credit because they want or need to buy something. They don’t want a mortgage; they want a home. Becoming customer-centric reframes what a bank can be and do for its customers. Then, you can tailor the ecosystem around customers’ needs and make the experience better overall.

NPSx founder Stanford Swinton discussed customer-centricity in financial services at XI Forum Europe 2022. Read the recap.

- Measure and improve. Relationship NPS (rNPS) measures customer satisfaction at regular intervals, and transaction NPS (tNPS) evaluates critical moments in the customer lifecycle. Put systems in place to track both and take quick, corrective actions if CX starts to slip.

You also need a path for feedback to reach operational teams. They need the data to improve and create more personalized and valuable experiences. Rapidly test and learn, so you know how strategies resonate with the customers you want to keep.

To stop customers from unbundling their banking services, financial institutions need to deliver simple, successful, and personalized experiences. Banks need to know their customers so well they can serve them better than anyone else.